DRL Over The Years

- 1984: Anji Reddy quits state-owned Indian Drugs & Pharmaceuticals (IDPL) to start DRL with Rs 25 lakh corpus

- 1986: DRL goes public and enters international

markets with methyldopa exports after IDPL stops producing drug owing to

technical reasons

- 1987: Becomes first Indian company to make its plant USFDA compliant, thus marking DRL’s foray into the world of generics

- 1991: Among early Indian companies to enter Russia, but opts for private pharmacies rather than traditional government route

- 1997: Licenses anti-diabetic molecule (Balaglitazone) to Novo Nordisk, validating Anji’s belief that research is the future of pharma

- 1999: Acquisition of American Remedies catapults DRL as the 5th largest Indian pharma company

- 2001: First Asia-Pacific (ex-Japan) entity to

list on NYSE, helping DRL not just raise money but also improve

transparency. Wins first patent challenge with 180-day marketing

exclusivity for generic drug (Fluoxetine 40 mg) in the US, giving DRL

confidence to build first-to-file pipeline and ushers in an era of

patent challenges

- 2005: Acquisition of Roche’s API business in Mexico helps DRL turn suppliers to innovators, a difficult market to crack until then

- 2006: Crosses $1 billion in revenues with the

acquisition of Betapharm in Germany, but change in regulations make

acquisition unviable

- 2007: DRL sees biosimilars as a growth area,

launches Reditux (Rituximab), the world’s first monoclonal antibody

biosimilar. Reditux goes on to be a market leader in its segment

- 2008: Post setback in research, DRL decides to

acquire technology platforms to strengthen R&D capabilities.

Acquires Dow Pharma’s small molecules business in the UK

- 2009: Strategic alliance with GSK for 100

products in emerging markets validates strength of product portfolio and

manufacturing capabilities

- 2011: Achieves critical size as revenues cross $2 billion, helping DRL take larger bets in product development

- 2012: Strengthens capabilities in injectables

and biosimilars through acquisitions and builds an impressive product

portfolio in each of its businesses following a deal with Merck Serono

and acquisition of Octoplus

***

There’s no larger-than-life portrait in the lobby but as soon as you

enter the swanky new corporate office of Dr Reddy’s Laboratories (DRL)

in Hyderabad’s posh Banjara Hills, your eyes land on what is perhaps the

perfect memorial to Anji Reddy, the company’s founder and the doyen of

the Indian pharmaceutical industry. It is DRL’s very own wall of fame,

etched with the name of every product India’s second-largest

pharmaceutical company has launched till date, including a slew of

blockbuster generic and branded launches such as Omeprazole, Fluoxetine,

Olanzapine, Sumatriptan, Simvastatin and Finasteride, among others,

which have helped the company become the multi-billion dollar behemoth

that it is today.

Kallam Anji Reddy was the son of a turmeric farmer in Andhra

Pradesh’s Guntur district. After finishing his education with a PhD in

chemical engineering from the National Chemical Laboratory in Pune, Anji

Reddy started his career with a stint at Indian Drugs &

Pharmaceuticals (IDPL) in 1969. He quit in 1975, became part of two

partnership firms for the next nine years and finally set up DRL with an

initial capital of Rs 25 lakh.

Since its inception in 1984, DRL is one of the few home-grown pharma

companies that has built a significant presence in some of the largest

markets around the world both in formulations and bulk drugs (also known

as active pharmaceutical ingredients, or API). Over the past decade,

revenues and net profit have grown from Rs 1,933 crore and Rs 251 crore,

respectively, in FY04, to Rs 11,626 crore and Rs 1,545 crore,

respectively, in FY 13. It is also a company that has always caught

trends early, be it the decision to move from bulk drugs to generic

formulations in the overseas market in 1990 or investing in new chemical

entity research as early as 1993.

|

|

|

|

“Anji Reddy was a visionary. Back in 1984, he spoke of DRL becoming a billion-dollar company"—B Parthasaradhi Reddy, Chairman, Hetero Drugs Group |

|

|

|

|

|

On

March 15, Anji Reddy died after a prolonged illness, and the mantle

passed formally to two men who sit at the top floor of this very modern,

steel-and-glass structure. Anji Reddy’s son-in-law, GV Prasad, and son,

Satish Reddy, couldn’t be more different. But they’ve been working

together for so many years now, their differences complement each other.

Prasad is the more reserved, plain-speaking leader who constantly

pushes the boundaries of what is possible; he is the big picture guy in

the company, identifying and investing in avenues for future growth such

as biosimilars and complex generics. Satish Reddy, who at 46 is younger

by seven years, is more open, a quick decision-maker and the go-to guy

for execution, scaling up operations in DRL’s key markets. Over the

years, Prasad, who is chairman and CEO of DRL, and Satish, the

vice-chairman and managing director, have learnt the ropes from Anji

Reddy and shaping DRL’s future based on its founder’s passion to

innovate and take on challenges. And it is clear that DRL, while staying

true to its founder’s vision, will now be making several changes to its

business model not only to adapt to the changing landscape of the

pharmaceutical industry but also seize upcoming opportunities across

geographies and products. “The fundamental DNA of the company is to

innovate, and that hasn’t changed,” declares GV Prasad. “Growth is the

agenda for the next two to three years. I want to see a shift in the

depth of innovation in all our businesses, which means our product

pipeline should be clearly differentiated from competition.” Putting

Europe and India back on track is also high on the DRL agenda. “Making

these markets perform as well as the others will be a priority,” he

adds. Will DRL’s new growth formulation work?

Making a mark

Anji Reddy’s guiding principle for business was to start something

where others felt “there was a battle to tackle”. That, combined with

his firm belief that any medicine Western pharma companies could

produce, Indians could produce at better quality and price, led him to

make DRL’s first API for the overseas market in 1986. At the time, IDPL

was about to stop making methyldopa because of a manufacturing glitch —

and what IDPL was wary of producing, no one in India would touch. Anji

Reddy promptly decided to start making methyldopa, telling the

then-managing director MP Chari that if the IDPL equipment lasted for

six months, they would make it work for two years. The gamble paid off

and DRL went on to the become the biggest supplier of methyldopa to

German pharma major Merck. The following year, after its plants got

USFDA approval, it began supplying ibuprofen to the US, and DRL was in

business.

|

|

|

| While GV Prasad is the big picture guy in the company, Satish Reddy is the go-to guy for execution |

|

|

|

|

|

In

2001, DRL was the first Indian company to get a 180-day marketing

exclusivity for anti-depressant Fluoxetine. The company raked in $56

million (Rs 258 crore) during the six-month period; more importantly, it

was the first step towards becoming a global generics player. In the

coming years, DRL built a pipeline of Para IVs (patent challenges) and

first-to-file (FTF) status, giving it 180-day exclusivity for products

such as Ondansetron for nausea in 2006, Olanzapine (20 mg) for

schizophrenia in 2011, and Finasteride for prostate problems and hair

fall in 2013, bringing in more than Rs 1,000 crore as revenue. It was

also the first generic company across the world to become an ‘authorised

generic supplier’, where it could market the drug partnering with the

innovator company without risk of litigation. Between 2006 and 2008, DRL

was the authorised generic supplier for Merck’s Zocar and Proscar and

Glaxo’s Imitrix, which earned the company over Rs 2,000 crore. “Dr

Reddy’s was one of the few companies to be successful overseas both in

API and formulation. Everybody was talking conceptually about how you

can sell in the US but it was only when companies such as Ranbaxy and

DRL executed their US strategy that smaller companies such as ours felt

confident about our foray,” says Rajeev Nannapaneni, vice-chairman and

CEO, Natco Pharma. The Hyderabad-based company currently supplies DRL

oncology drugs in the Indian market.

Certainly, DRL’s success served as inspiration for others to start on

their own. B Parthasaradhi Reddy, the chairman of the Hetero Drugs

group, is very proud that he was one of the first employees at Dr

Reddy’s Laboratories (DRL). “I began my career under Anji Reddy and

everything I learnt in this business is because of him,” he says.

Parthasaradhi first worked with Anji Reddy at Uniloids in 1979 as a

research trainee and moved to head research at DRL in 1984 after a brief

stint at another Anji Reddy company, Standard Organics. “Back in 1984,

he would talk about how DRL would become a multi-billion dollar company —

at a time when Rs 100 crore of revenue was considered huge. That was

the kind of visionary he was.” Parthasaradhi left DRL in 1993 to set up

his own pharma company but his connect with the company remained strong.

“I continued to watch and learn even from the outside.”

He is one of several pharma company promoters who have been inspired

to entrepreneurship thanks to DRL — Aurobindo Pharma’s Ram Prasad Reddy,

Divi Lab’s Murali K Divi and Raghvendra Rao of Orchid Pharma all either

worked with Anji Reddy or struck out on their own after seeing his

track record.

Exclusive generics

If Anji Reddy was the quintessential risk-taker, Prasad is credited

with driving the core operations of the company, transforming DRL from a

mid-sized pharma company to a global player. And Satish excels at

execution, spearheading the company’s move over the past several years

from being API-focused to becoming a branded formulations player.

|

|

|

|

“All their [DRL’s] strategic decisions have been centred on the optimal use of capital rather than chasing scale"—Prashant Nair, Deputy head of research, Citi India |

|

|

|

|

|

As

a result, while global generics continue to be DRL’s mainstay,

contributing 71% of overall revenues, what has changed is the company’s

focus. Over the past four years, the business has grown nearly

three-fold to $738 million, driven by key product launches such as

Fondaparinux, Sumatriptan, Atorvastatin, Tacrolimus and Olanzapine. “A

large part of our portfolio was dependent on Para IVs and FTFs. We have

not given that up, but our priorities have changed: we are focusing now

on limited competition products where we have some advantage on

technology,” points out Satish Reddy.

Limited competition products are generics that could be off-patent

but are complicated, with a higher technological component; they are

either in niche therapeutic areas or delivered differently in, say,

topical or injectable forms. Currently, DRL has a pipeline of 200 ANDAs

(abbreviated new drug application, an application for introducing a

generic version of a branded drug that is coming off patent in the US).

According to Prashant Nair, deputy head of research, Citi India, about a

third of the company’s future ANDA filings are for products with a high

technology threshold, where competition could be limited. “This should

help the company differentiate itself in the US pharma market,” he adds.

There

will also be a cost advantage: unlike in Anji Reddy’s time, the core

generics business is witnessing cut-throat competition and price erosion

after the exclusivity period is as high as 90-95% in some products.

In complex generics, limited competition means price erosion is only

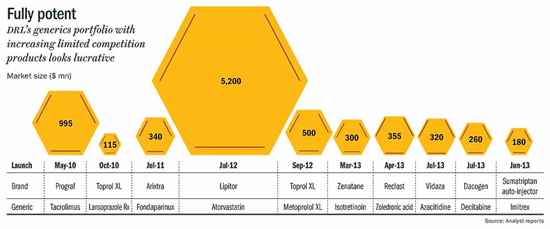

about 30-35%. At DRL, revenue from limited competition products is

expected to increase from $238 million (Rs 1,428 crore) in FY13 to $438

million (Rs 2,628 crore) over the next two years, driven by the generic

launches of Reclast, Zometa, Dacogen as well as Vidaza (see: Fully

potent).

What is DRL’s strategy for moving beyond plain vanilla generics? It

is first focusing on building capabilities. “We are aggressively looking

for opportunities to acquire capabilities in limited competition

products,” says Satish Reddy, pointing to the Octoplus acquisition as a

case in point. “You will see more such moves that will shorten the time

in developing our capabilities,” he adds. In October 2012, DRL paid

€27.4 million to acquire the Netherlands-based Octoplus to augment its

focus in the injectables segment. The injectables market is valued at

$2.8 billion, and some of DRL’s filings in this segment include the

$2.9-billion multiple sclerosis drug Copaxone and $500-million

anticoagulant Angiomax. Generic versions of both drugs are expected in

mid-2015 and the prospects are attractive since no other company has

filed to offer a generic version.

For Russia, with love

Another important part of the company’s growth engine are the

emerging markets. DRL’s focus on emerging markets isn’t a new move for

the company — while the company is present in countries such as South

Africa, Venezuela, Australia, New Zealand, Vietnam, Myanmar and Sri

Lanka, Anji Reddy had a soft spot for Russia. He said the former USSR

had helped the Indian pharma industry considerably in its early stages:

when he was with IDPL, there was much technology transfer from Russia to

develop medicines here and make healthcare affordable. DRL’s founder

felt the burden of debt and in 1998, demonstrated his commitment to

Russia by staying put even through the rouble crisis.

|

|

|

|

“It

will be an uphill task for Dr Reddy’s to get ahead of its peers in the

Indian market. It takes time to scale up individual brands"—Hemant Bakhru, Analyst, CLSA |

|

|

|

|

|

Like

Anji Reddy, Prasad and Satish pay extra attention to Russia and it

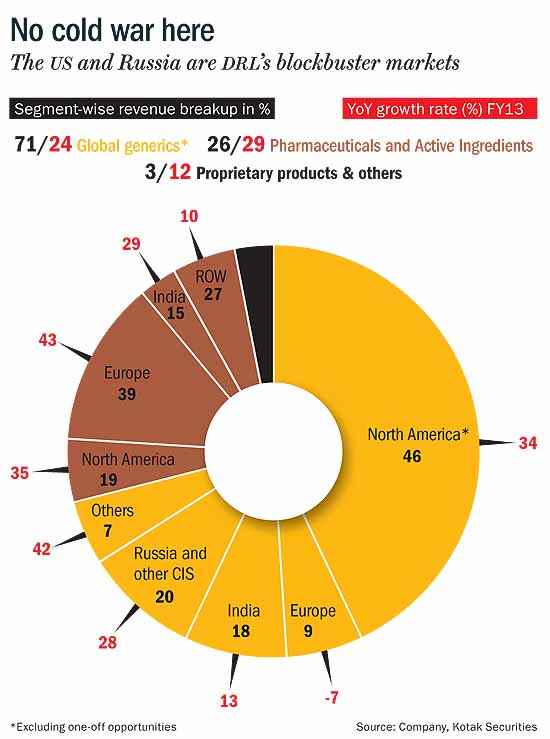

returns the interest. In FY13, Russia contributed Rs 1,400 crore to

DRL’s topline and since 2009, the market has grown steadily at an

average 20%, driven by its major brands in the prescription segment and

the impressive growth of some of its new brands in the OTC portfolio,

whose contribution has increased from 13% to 34% of overall sales (see:

No cold war here). “Dr Reddy’s was able to anticipate that the brands in

the prescription segment are likely to see pricing pressure from the

[Russian] government, which is now telling doctors to prescribe generic

products. So, they decided to scale the OTC business,” points out Hemant

Bakhru, analyst at CLSA.

Now, the dynamics of the Russian market are changing. While the

mandate to prescribe generic drugs instead of brands products wherever

substitutes are available is a positive for DRL, there is also an import

substitution bill in the offing, which if passed, will require foreign

generic and innovator companies to have a manufacturing presence in

Russia. “We are watching how the situation evolves,” says Prasad, adding

that the company is willing to invest in local manufacturing facilities

if required. In addition, DRL is also looking to not only acquire

brands to augment its product portfolio but also make in-licensing deals

such as the one with Cipla where it has marketing exclusivity for some

Cipla OTC brands in Russia and Ukraine.

Meanwhile, another deal, with GlaxoSmithKline Pharma in 2009, is

expected to drive emerging market revenue in the next three to four

years. Already, revenue from other emerging markets has grown nearly

three times from over Rs 195 crore in FY09 to Rs 553 crore in FY13. The

GSK Pharma deal covers 100 products and intends to tap emerging markets

stretching from Asia Pacific to Latin America. Products will be made by

DRL and licensed to GSK, which will file registrations and distribute

them either singly or with DRL in the chosen markets. India isn’t part

of the deal. But then, India is a whole ’nother story in any case.

A passage to India

Despite its success in the US and other markets, or perhaps because

of it (at least, to some extent), DRL is still not a big player in

India. Ironically, the country’s second-largest pharma company isn’t in

the top 10 in the domestic pharma market. “We have lagged behind in our

peformance in the domestic market,” agrees Prasad. “We have done a

number of things to fix that and have come back to industry-plus growth

rates, but that is still not adequate.”

|

|

|

| Despite its success in the US and other markets, or perhaps because of it, DRL is still not a big player in Indian pharma |

|

|

|

|

|

It’s

understandable why Dr Reddy’s wanted to focus on the US market — it

made sense to focus on scaling up operations in the world’s largest

generics market. But there’s no denying that the decision took attention

away from the home market. Also, DRL gets a large chunk of its revenue

from acute therapies, which aren’t growing as fast in India as chronic

drugs. And, unlike companies such as Sun Pharma and Cipla, which flooded

the market with several new products, DRL has focused on a few selected

brands. For sure, that turned some of its products such as Omez, Nise

and Ciprolet into market leaders, but the limited portfolio meant it

lagged in market share.

Now, Satish and Prasad are working to correct that. In the past four

years, the sales force has been beefed up by over 50% to 4,600 and

marketing has been expanded to rural areas. DRL has also focused on new

product launches and line extensions of its key brands on

gastrointestinal, cardiovascular, pain management and oncology

therapies, which account for 60% of its revenues. That has helped the

company grow in line with the market average of 14% between FY09 and

FY13 (after hitting a low of 5% in 2009), but the path ahead remains

challenging. “It will be an uphill task for Dr Reddy’s to get ahead of

its peers in the Indian market. It takes time to scale up individual

brands because you need to gain acceptance from the medical community,

which happens only gradually. India is not like the US where you can

launch a blockbuster generic and gain significant market share

overnight,” points out CLSA’s Bakhru.

As with other markets and its strategy for specialised generics,

here, too, DRL is considering acquisitions — individual brands as well

as entire portfolios — as a way to rapidly gain scale and market share.

“The market has no room for so many players. The entry of MNCs has

raised the expectations of valuations, but at some point of time,

consolidation will happen. Increasingly, smaller players will find it

difficult to keep up as costs are going up and they don’t have a large

portfolio. We are waiting for valuations to reach reasonable levels,”

says Satish Reddy. Recently, DRL walked away from the Mumbai-based Elder

Pharmaceuticals since it felt the bids for the debt-ridden company were

too high.

Banking on biosimilars

Acquisitions aside, what may help drive growth in India over the long

term is DRL’s biosimilars business. Biosimilars are generic equivalents

of biotech drugs, such as insulin, growth hormones etc. In 2007, DRL

launched Reditux in India, the first biosimilar monoclonal antibody

(which makes it easier for the immune system to find cancer cells by

attaching itself to parts of the cancer cell); currently, the drug holds

65% market share. In the past five years, the company has launched four

more biosimilars, with another seven in the pipeline. “There is no one

in the domestic industry that is really launching novel products and Dr

Reddy’s can leverage its efforts in product development in biosimilars

to fill that gap,” says Kewal Handa, promoter, Salus Lifecare, who

earlier headed the Indian business of American pharma giant Pfizer.

|

|

|

|

“No one is launching novel products in the domestic industry and Dr Reddy’s can fill that gap in the market"—Kewal Handa, Founder, Salus Lifecare |

|

|

|

|

|

Globally,

the biosimilars market is expected to cross $4-6 billion by 2016 from

the current $2 billion. To tap into this potentially lucrative market,

DRL entered into a partnership with Merck Sereno, a division of Merck,

to develop and commercialise biosimilar products in oncology, primarily

focused on monoclonal antibodies. Such an alliance allows DRL to

mitigate the risks involved in developing a biosimilar — the cost is

pegged at $100-200 million, with 70% going towards clinical development.

“While product launches in biosimilars in the developed market is still

some time away, DRL will have the first mover’s advantage among Indian

companies, given the investment the company has already made and the

high entry barriers in the business as it takes time to develop

capabilities,” says Krishna Prasad, analyst at Kotak Institutional

Equities. In the past five years, the company has invested over Rs 3,600

crore to increase capacity in its existing facilities and create new

capacities in oral solids, injectable facilities and biosimilars.

Bitter pill

If DRL is in the pink of health now, it’s also had its share of bad

medicine. The lessons learnt from those missteps have shaped the

company’s strategy for the future. For instance, when the going was

good, DRL expanded to nearly 48 countries, including Brazil, Mexico and

Japan. With the 2008 meltdown, though, it packed up operations in more

than 30 markets. “We were in so many markets that it created complexity

in operations. Instead, we streamlined our operations so there would be

more predictability in revenues rather than be present in many

countries,” says Satish Reddy.

|

|

|

| Inlike companies such as Cipla and Sun pharma, DRL has focused on a few brands |

|

|

|

|

|

Then

there’s the Betapharm acquisition. In 2006, DRL paid $560 million for

the German generic drug maker, the largest buyout by an Indian pharma

company. It seemed like a good idea at the time: Germany was the

second-largest generics market after the US. But things unravelled soon

after, when the German government allowed procuring of generics through

tenders; health insurers began procuring medicines from vendors with

the lowest bids, leading to massive price erosion. DRL finally had to

write off nearly half its investment; it brought down the workforce from

400 to 80 people and transferred the manufacturing to India. Despite it

not being the highest bidder, DRL walked away with the deal that took

85 days to clinch because the promoters of Betapharm felt the business

fit between both companies would be better. While it did seem the deal

put DRL ahead of its peers in Germany, there were concerns even at the

time that it was too expensive. “There was a fair bit of aggressive

bidding by all the companies in the fray, including Ranbaxy, Teva,

Sandoz, Wockhardt and Nicholas Piramal. I think Dr Reddy’s did get

carried away because the deal also brought it closer to its $1 billion

revenue target for 2008,” says an analyst on condition of anonymity.

Cutting Edge: DRL’s buyout of Dow Pharma’s small molecules business has beefed up its research capabilities

Cutting Edge: DRL’s buyout of Dow Pharma’s small molecules business has beefed up its research capabilities

Now, looking back, Satish Reddy admits, “Germany didn’t work out the

way we wanted. Now, our focus is shifting from the tender business to

specialty products but you have to give it some time before we get our

act together. Our European strategy is still evolving because the market

itself is changing.”

|

|

|

| After the Betapharm experience, DRL is not seeking scale, but is instead looking at strategic capability fits |

|

|

|

|

|

While

Betapharm was a failed buy, it did bring some valuable lessons. First,

the acquisition made Prasad and Satish Reddy realise that chasing scale

is not always a successful strategy. “Today, we are acquiring smaller

companies that add to our capabilities. We are not acquiring for scale,”

confirms Prasad. The Octoplus buy is a perfect example of the changed

focus, as is the 2008 acquisition of Dow Pharma’s small molecules

business in the UK and 2011’s buy of GSK’s penicillin facility in the

US. While Dow Pharma augmented DRL’s manufacturing and research

capabilities in its custom pharmaceutical services business, the GSK

business resulted in additional revenues through brands such as

Augmentin and Amoxil. “All their strategic decisions have been centred

on optimal use of capital rather than chasing scale,” says Nair of Citi.

Spotlight on research

Another change at DRL is its changed focus on research. Back in

1993-94, Anji Reddy started a research arm at DRL, the first Indian

company to do so. It was also the first company to out-license a

molecule, Balaglitazone, to Novo Nordisk in 1997. The molecule is named

after Balaji, the presiding deity at Tirupati. But, interestingly, it

wasn’t Anji Reddy’s first choice, who wanted to name it Venglitazone

after Lord Venkateswara, the more formal name of Balaji. But the World

Health Organisation rejected it since it would clash with another

molecule, Englitazone.

|

|

|

|

“We will see India emerge as a strong contender on the innovation side once it establishes its foothold in the generics world"Glenn Saldahna, MD, Glenmark |

|

|

|

|

|

In

1998, DRL out-licensed another diabetes molecule, Ragaglitazar, to Novo

Nordisk and a third molecule to Novartis Pharma in 2001 for $55

million. But all of them were eventually discontinued as the results

from clinical trials were unsatisfactory. “Getting a new molecule to

market is a huge challenge. More than 90% of molecules that enter trials

fail because the human body is never fully understood. Research is a

difficult game because you need deep pockets and deep understanding of

the science,” says Prasad.

Glenn Saldahna, managing director of another Indian pharma company

Glenmark, agrees with Prasad. “It took even Japan a couple of decades to

become a destination for innovation. The momentum is building and we

will see India emerge as a strong contender even on the innovation side

after establishing its foothold in the generics world,” he says

optimistically. Glenmark, too, has out-licensed three molecules and

already raked in over $200 million as a result.

What is the big change at DRL when it comes to research? It is

focusing on areas where the risk is lower and the translation from lab

to commercial products is higher. When DRL started research in 1993, it

chose diabetes and cardiovascular therapy as its areas of focus, given

that India has the largest diabetic population in the world. But, given

the huge costs and low success of its clinical trials, it has moved away

from those two areas, into anti-infectives, pain management and

dermatology. In addition, the company is now also looking at incremental

innovation, which means taking an existing molecule and changing the

way it is delivered. It currently has 21 proprietary products in the

pipeline, of which six are in clinical development in the areas of pain

management, psoriasis and migraine.

At the same time, DRL is also spending more on research than ever

before. In FY13, the company invested Rs 790 crore on R&D, 34% more

than the Rs 591 crore it spent the previous year. That’s also a lot more

than other Indian pharma companies. In FY13, Ranbaxy spent Rs 450

crore, Sun Rs 676 crore and Lupin, Rs 710 crore. “Since we have achieved

considerable scale in revenues, we are able to take larger bets on

research,” says Prasad.

Certainly, the numbers at DRL are looking good. Revenues grew from Rs

6,944 crore in FY09 to Rs 11,626 crore in FY13 and operating margins

(excluding FTF sales) saw an impressive improvement from 16% to 20.3%

over the same period, thanks to increasing contribution of complex

generic products. Analysts expect revenues to increase to Rs 17,479

crore in FY16, with operating margins climbing further to 22.5%. As a

consequence, net profit should rise from Rs 1,545 crore last year to Rs

2,670 crore in FY16. While the business continues on the growth path,

Anji Reddy’s successors haven’t forgotten his dream. “He was really

driven by challenges and things done for the first time. Drug discovery

was his passion — he wanted DRL to be the first Indian company to take a

molecule from lab to global launch,” says Prasad. “In his last months,

he used to call this his ‘unfinished agenda’.” If Prasad and Satish

Reddy manage to fulfil that dream, it will be a fitting tribute.

Exclusive generics

Exclusive generics

There

will also be a cost advantage: unlike in Anji Reddy’s time, the core

generics business is witnessing cut-throat competition and price erosion

after the exclusivity period is as high as 90-95% in some products.

There

will also be a cost advantage: unlike in Anji Reddy’s time, the core

generics business is witnessing cut-throat competition and price erosion

after the exclusivity period is as high as 90-95% in some products.

No comments:

Post a Comment